#Synthetic Rope market Growth

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

12.7% of mobile users access Tumblr.

Text

Offshore Mooring Market Drivers: Growing Deepwater Exploration and Rising Energy Demand

The offshore mooring market is experiencing significant momentum, propelled by the rapid expansion of offshore oil and gas exploration, particularly in deepwater and ultra-deepwater regions. As global energy demands surge and conventional hydrocarbon reserves dwindle, companies are venturing farther into the oceans, necessitating robust and reliable mooring systems to anchor floating production units. Additionally, the expansion of offshore renewable energy installations, especially wind farms, has added a new dimension to the market, creating fresh avenues for growth.

Rising Offshore Exploration in Deep and Ultra-Deep Waters

One of the key drivers of the offshore mooring market is the increase in exploration and production (E&P) activities in deeper water bodies. With easy-to-reach onshore and shallow water oil reserves declining, oil companies are investing in deep-sea projects to meet future energy demands. Deepwater projects demand advanced mooring systems that can handle higher pressures, greater water depths, and more intense weather conditions. These complexities drive innovation in mooring technologies and materials, pushing demand for high-performance anchoring solutions like taut leg, spread mooring, and dynamic positioning systems.

Furthermore, national oil companies and energy majors are aggressively pursuing exploration programs in regions like the Gulf of Mexico, Brazil's pre-salt basin, and the North Sea. These areas are known for their challenging underwater terrain and operational risks, which in turn drive up the need for reliable and advanced mooring infrastructure.

Growing Offshore Wind Energy Installations

The global shift toward cleaner energy sources is boosting offshore wind power development, which directly impacts the offshore mooring market. Offshore wind farms, especially floating wind turbines deployed in deep waters, require sophisticated mooring systems to remain stationary. Countries such as the UK, Norway, China, and Japan are significantly expanding their offshore wind capacity, often in deeper waters where fixed-bottom foundations are impractical. Floating offshore platforms need adaptable and corrosion-resistant mooring systems that can withstand changing sea states and dynamic loads.

As governments increase their investments in green energy to meet carbon reduction targets, the role of offshore mooring in supporting floating wind technology becomes more vital, paving the way for market expansion beyond traditional oil and gas applications.

Technological Advancements and Customization

Advancements in material sciences, hydrodynamic analysis, and simulation technologies have revolutionized mooring system design. Innovations like synthetic fiber ropes, hybrid mooring systems, and automated tension monitoring allow for greater efficiency and safety in offshore operations. These developments are especially critical in ultra-deepwater environments, where environmental loads are unpredictable.

The growing demand for customized mooring solutions tailored to specific offshore conditions has also led to a surge in R&D investments. Companies are increasingly offering flexible, cost-efficient, and sustainable mooring systems to cater to diverse offshore project requirements, thus driving market growth.

Expansion of FPSO and FLNG Units

Floating production storage and offloading (FPSO) units and floating liquefied natural gas (FLNG) facilities are being widely adopted to optimize offshore hydrocarbon production. These floating units require complex mooring systems capable of holding them securely in place during various operational stages. As FPSOs become more popular in deepwater and marginal fields due to their cost-effectiveness and deployment flexibility, the offshore mooring market benefits directly from their proliferation.

In addition, the increasing deployment of FLNG vessels, which enable liquefaction of natural gas at sea and reduce the need for onshore infrastructure, further drives the demand for specialized mooring solutions capable of handling high loads and extreme environmental conditions.

Stringent Safety and Environmental Regulations

Government bodies and environmental organizations worldwide are enforcing stricter regulations for offshore infrastructure, ensuring safer and environmentally responsible operations. These regulations mandate the use of high-quality, certified mooring components that minimize environmental damage and withstand operational stresses. In response, operators are upgrading existing mooring systems or adopting state-of-the-art solutions, stimulating demand in the aftermarket and replacement segments.

Moreover, safety incidents and oil spills have made stakeholders more cautious about the mooring systems' integrity and reliability. This shift is compelling industry players to prioritize quality, precision, and compliance in mooring system deployment and maintenance.

Conclusion

The offshore mooring market is being steered by a confluence of drivers ranging from deepwater exploration to renewable energy adoption. As offshore infrastructure becomes increasingly complex and essential to global energy supply chains, the demand for advanced, reliable, and environmentally compliant mooring systems continues to escalate. Companies that focus on innovation, regulatory adherence, and project-specific customization are well-positioned to capitalize on the accelerating growth in this high-stakes, technologically driven market.

0 notes

Text

Nylon Filament Yarn Market Set for Global Growth Surge

The Nylon Filament Yarn Market is set to witness robust growth over the coming years, driven by rising demand from industries such as textiles, automotive, and industrial manufacturing. Known for its strength, elasticity, and durability, nylon filament yarn continues to be a material of choice across a variety of high-performance applications.

From fashion and sportswear to airbags and tire cords, nylon filament yarn has established itself as a versatile and indispensable component. Global market trends indicate strong momentum as manufacturers increase production capacity, driven by demand for lightweight and high-strength materials.

Dataintelo’s latest research highlights that the market is projected to register substantial growth through 2032, supported by technological advancements, sustainability trends, and increasing usage in developing regions.

Key Drivers Fueling Market Growth

Several pivotal factors are driving the expansion of the Nylon Filament Yarn Market:

Rising Textile Consumption: As global fashion and apparel consumption increases, especially in emerging economies, nylon yarns are being widely used in woven and knitted fabrics due to their superior strength and wrinkle resistance.

Automotive Sector Demand: With growing automobile production, particularly in Asia-Pacific, nylon filament yarn is increasingly used in tire reinforcement, safety belts, and airbags due to its high tensile strength.

Sportswear and Activewear Trends: The ongoing popularity of active lifestyles and performance-oriented clothing is spurring the use of lightweight, moisture-wicking fabrics made with nylon filament yarn.

Technological Advancements: Innovations in spinning and texturing technologies are enhancing product performance and expanding its use across niche segments.

Challenges and Restraints in the Market

Despite the positive outlook, the market faces some notable restraints:

Fluctuating Raw Material Prices: Since nylon filament yarn is derived from petrochemical products, price volatility of caprolactam and other raw materials can impact production costs.

Environmental Concerns: Nylon is a synthetic polymer that raises sustainability concerns due to its non-biodegradable nature and energy-intensive production process.

Market Competition: Increasing availability of alternative synthetic fibers like polyester may challenge the market share of nylon filament yarn in some regions.

Request a Sample Report https://dataintelo.com/request-sample/197593

Opportunities Steering Market Potential

The Nylon Filament Yarn Market is witnessing several transformative opportunities:

Eco-Friendly Innovations: The development of bio-based and recycled nylon yarn is gaining traction, especially in sustainable fashion initiatives.

Expansion in Technical Textiles: Nylon filament yarn is increasingly being used in industrial and technical applications like geotextiles, ropes, and conveyor belts, providing long-term market stability.

Rising Investment in Emerging Markets: Growing manufacturing bases in countries like India, Vietnam, and Indonesia are expanding nylon production and opening new regional opportunities.

Global Market Insights and Trends

Across regions, Asia-Pacific dominates the global Nylon Filament Yarn Market owing to:

High textile production in China and India

Expanding automotive and infrastructure sectors

Cost-effective labor and raw material availability

Meanwhile, North America and Europe are witnessing steady demand, driven by their advanced automotive industries and growing emphasis on sustainable textile production.

View Full Report https://dataintelo.com/report/global-nylon-filament-yarn-market

Market Segmentation Snapshot

The market can be categorized based on the following segments:

By Type:

Fully Drawn Yarn (FDY)

Partially Oriented Yarn (POY)

High Tenacity Yarn

Others

By Application:

Apparel & Textiles

Automotive

Industrial

Others (Home Furnishings, Carpets, etc.)

By Region:

North America

Europe

Asia-Pacific

Latin America

Middle East & Africa

Each of these segments offers unique growth prospects, with FDY leading due to its wide use in clothing, while high tenacity yarn is gaining popularity in industrial applications.

Growth Forecast and Value Outlook

The Nylon Filament Yarn Market is expected to maintain a steady compound annual growth rate (CAGR) from 2023 to 2032. The market value is projected to reach multi-billion-dollar levels during the forecast period, driven by widespread application and innovation.

Notably, the industrial yarn segment is forecasted to grow at a higher pace due to its use in technical textiles and automotive applications. In contrast, apparel and sportswear segments continue to dominate the consumption landscape.

Check Out the Report https://dataintelo.com/checkout/197593

Competitive and Strategic Landscape

While specific company names are excluded as per guidelines, it’s worth noting key strategies that are shaping the market landscape:

Product Innovation: Emphasis on developing flame-retardant, antibacterial, and UV-resistant yarns.

Capacity Expansion: Manufacturers are expanding production capabilities to meet rising global demand.

Sustainability Initiatives: Investment in circular production and bio-based yarns to address environmental concerns and regulatory pressures.

Future Outlook and Market Dynamics

The Nylon Filament Yarn Market is transitioning from traditional uses toward more advanced and sustainable applications. The introduction of greener alternatives and efficient production processes are expected to redefine the competitive dynamics.

With regulatory focus increasing on reducing carbon emissions in textile production, the market is likely to see more R&D in low-impact manufacturing technologies and recyclable yarn solutions.

Explore the Report in Detail https://dataintelo.com/report/global-nylon-filament-yarn-market

Conclusion

In conclusion, the Nylon Filament Yarn Market presents a promising growth trajectory fueled by rising demand in textiles, automotive, and industrial applications. Innovations in sustainable yarn production, expanding global supply chains, and shifting consumer preferences toward performance fabrics are expected to play a pivotal role in shaping the future of the market.

0 notes

Text

Ropes Market insights reveal new trends shaping the global demand and supply chain

Understanding the Ropes Market: A Shift in Global Trends

The Ropes Market has experienced a notable evolution in recent years due to shifting global dynamics. With rising applications in construction, shipping, oil and gas, mining, safety gear, and sports industries, the demand for both synthetic and natural ropes is growing steadily. In response to this demand, manufacturers are adopting new strategies to align with customer expectations and modern logistics systems.

As companies strive for increased operational efficiency, they are increasingly investing in innovative rope solutions, contributing to significant transformations across the global supply chain. In this article, we explore the latest market insights, trends, and factors impacting the global ropes market today.

Rise in Demand Across Diverse Industries

The ropes market is witnessing growing demand from diverse industries. Marine and offshore sectors require high-strength synthetic ropes for mooring and towing. The construction industry depends on durable ropes for lifting, rigging, and securing loads, while the oil and gas sector needs robust solutions for extreme conditions.

Another emerging area is the sports and leisure segment, where climbing ropes, gym ropes, and boating ropes are seeing increased use. This diversification of applications is widening the global market base and driving innovation in rope materials and design.

Supply Chain Evolution Driven by Globalization

The global nature of the ropes market necessitates a streamlined and resilient supply chain. Manufacturers are now investing in automation, real-time inventory tracking, and regional warehousing to avoid bottlenecks. Additionally, geopolitical uncertainties and raw material shortages are pushing companies to reassess and diversify their sourcing strategies.

Rope manufacturers are also partnering with local suppliers to reduce lead times and maintain consistent quality, leading to the emergence of hybrid supply chain models that balance efficiency with risk mitigation.

Innovation in Rope Materials and Manufacturing

Innovation plays a critical role in shaping the ropes market. The shift from traditional fibers like manila and sisal to high-performance materials such as UHMWPE (ultra-high-molecular-weight polyethylene), aramid fibers, and polyester has redefined performance expectations. These synthetic ropes offer greater strength-to-weight ratios, improved durability, and resistance to weather and chemicals.

Automation and digital manufacturing are further enhancing production capacity and quality. Technologies such as precision braiding and advanced coating methods are ensuring consistent rope performance across demanding environments.

Regional Trends and Consumption Patterns

North America and Europe remain key markets due to high safety standards and heavy industrial usage. However, the Asia-Pacific region is emerging as a major growth area, thanks to expanding infrastructure projects in countries like India and China. This surge in construction and shipping activities is translating into increased demand for both standard and customized rope solutions.

Latin America and Africa, while smaller in size, present future potential due to growing investments in mining and oil exploration, further broadening the global demand footprint.

Sustainability and Eco-Conscious Manufacturing

Sustainability is no longer a secondary concern—it’s becoming central to manufacturing decisions in the ropes market. Consumers and industries alike are showing preferences for biodegradable and recyclable ropes. In response, companies are experimenting with eco-friendly materials and processes that reduce environmental impact without compromising on strength or durability.

Some manufacturers are even integrating circular economy practices, reusing fibers from end-of-life ropes and reducing waste through closed-loop systems.

Digital Integration and Smart Logistics

The ropes market is also witnessing the integration of digital tools into logistics and supply chain management. With IoT-based inventory systems, predictive maintenance for production equipment, and AI-powered demand forecasting, businesses can ensure timely deliveries and reduce inventory losses.

Digital platforms are enabling end-to-end visibility across global trade routes, allowing manufacturers to respond quickly to disruptions such as port delays or raw material shortages.

Impact of Economic Fluctuations on the Supply Chain

The global supply chain for ropes remains sensitive to economic shifts. Rising freight costs, inflation, and exchange rate volatility have led to unpredictable pricing and availability. To combat this, suppliers are entering into long-term contracts and increasing local sourcing to shield themselves from global price fluctuations.

In regions with unstable currencies, rope manufacturers are adjusting pricing strategies or seeking alternative trade routes to minimize disruptions.

Conclusion: A Market on the Move

The ropes market is undergoing a significant transformation, shaped by innovation, digitalization, and shifts in global trade patterns. As demand diversifies and supply chains evolve, companies that invest in advanced materials, regional manufacturing hubs, and sustainable practices are well-positioned to lead.

Understanding these ongoing changes is essential for stakeholders seeking to navigate the future of this dynamic and essential market.

#ropesmarket#supplychaintrends#syntheticrope#constructionindustry#maritimesector#sustainability#industrialmaterials#globaltrade#ropemanufacturing#marketinsights

0 notes

Text

Steel Wire Rope Market Overview: Global Trends and Forecast 2025–2030

The steel wire rope market is poised for significant growth between 2025 and 2030, driven by industrial expansion, infrastructural development, and the increasing need for high-performance materials in various sectors. Steel wire ropes, known for their strength, flexibility, and durability, are used in applications ranging from construction to marine operations, mining, elevators, and oil and gas industries. As global demand for heavy lifting, secure transportation, and robust infrastructure rises, so does the importance of this versatile product.

Global Trends Shaping the Market

Several global trends are influencing the trajectory of the steel wire rope market. One of the most notable is the steady growth in urbanization, especially in emerging economies such as India, China, Indonesia, and Brazil. Urbanization leads to increased construction activities, infrastructure upgrades, and a higher demand for lifting and hoisting solutions — all of which are heavily reliant on steel wire ropes.

Moreover, sustainability is becoming a central theme across industries. Manufacturers in the steel wire rope market are investing in recyclable materials, eco-friendly production methods, and innovative coatings that reduce environmental impact while increasing product lifespan.

Forecast Growth Drivers (2025–2030)

From 2025 to 2030, several drivers will fuel the growth of the steel wire rope market:

Construction and Infrastructure Expansion: The rising demand for high-rise buildings, bridges, ports, and transport networks is directly boosting the need for steel wire ropes used in cranes, elevators, and suspension systems.

Maritime and Offshore Applications: As global trade and offshore drilling expand, there’s an increasing requirement for ropes with high tensile strength and corrosion resistance, particularly in saltwater environments.

Mining and Heavy Equipment: The mining sector continues to be a major consumer of steel wire ropes, especially for draglines, shovels, and hoisting systems. Countries with resource-rich regions are expected to be hotspots for growth.

Technological Advancements: New developments in material engineering have led to lightweight yet strong steel wire ropes with better fatigue resistance, making them suitable for extreme operational environments.

Emerging Economies: Asia-Pacific and Latin America are seeing substantial investments in industrial and public infrastructure, creating new avenues for market penetration.

Key Regional Insights

North America: Focused on infrastructure renewal and industrial automation, with rising investments in oil & gas exploration.

Europe: Driven by strict safety regulations, technological innovation, and a mature construction sector.

Asia-Pacific: The largest and fastest-growing region, led by China and India due to booming construction and manufacturing sectors.

Market Challenges

Despite a promising future, the steel wire rope market is not without challenges. The most significant issue is the volatility in raw material prices, particularly steel. Global trade tensions and supply chain disruptions can also impact pricing and availability. Moreover, competition from synthetic ropes in certain applications may limit growth unless manufacturers continue to innovate.

Competitive Landscape

The steel wire rope market is moderately consolidated, with a mix of global players and regional manufacturers. Companies are focusing on mergers, acquisitions, and strategic partnerships to strengthen their global footprint. Innovation, product quality, and customer-specific solutions remain the core competitive differentiators.

Innovations and Future Outlook

Innovation is key to the future of the steel wire rope market. Trends like high-performance coatings, hybrid wire rope structures, and digital monitoring systems for wear and tear are gaining popularity. Additionally, integration with smart systems and predictive maintenance tools is expected to redefine product lifecycles and safety standards.

By 2030, the steel wire rope market is expected to evolve into a more tech-driven and environmentally conscious industry. The adoption of smart manufacturing processes and the development of sustainable, high-strength ropes will continue to drive competitive advantages and open new market segments.

Conclusion

The steel wire rope market is on a clear growth path, fueled by industrial demand, infrastructural advancements, and technological innovations. As the world gears up for more complex and large-scale projects, steel wire ropes will remain indispensable in ensuring safety, efficiency, and durability across industries. From 2025 to 2030, stakeholders can expect not only growth in volume but also an evolution in the quality and versatility of steel wire ropes, tailored to meet the challenges of the modern world.

0 notes

Text

National Ropes and the Rise of Quality Rope Manufacturing in India

India has long been known for its thriving industrial sector, and among the many industries seeing rapid growth is the rope manufacturing industry. As demand for high-quality ropes continues to rise in sectors such as shipping, construction, oil & gas, and agriculture, the need for reliable rope manufacturers has never been more important. One name that consistently stands out among the top ropes manufacturers in India is National Ropes — a brand known for its durability, innovation, and commitment to quality.

The Importance of Rope Manufacturing in India

Ropes are more than just industrial tools — they are critical to the safety and efficiency of countless operations. Whether it's used in a cargo ship, a construction crane, a mountain rescue mission, or a rural farming application, the right rope can make all the difference. That’s why India has invested significantly in rope production technologies, creating a space for manufacturers like National Ropes to thrive.

As one of the reputed ropes manufacturers in India, National Ropes is leading the charge with cutting-edge production standards, wide product variety, and a strong commitment to customer satisfaction.

Why National Ropes Stands Out

National Ropes has earned a reputation for excellence in both domestic and international markets. What sets them apart is their attention to detail and adherence to quality control processes. Whether you're looking for steel wire ropes, synthetic fiber ropes, or customized rope solutions for specialized industries, National Ropes offers it all.

Their manufacturing facilities are equipped with the latest machinery, enabling them to produce ropes that meet global standards. Each product is rigorously tested for strength, durability, and resistance to environmental conditions, ensuring that clients receive only the best.

Wide Range of Applications

National Ropes caters to a broad spectrum of industries, including:

Shipping and Marine: High-tensile, corrosion-resistant ropes that withstand harsh marine environments.

Oil & Gas: Heavy-duty steel ropes used in drilling and offshore applications.

Construction: Wire ropes used in cranes, elevators, and scaffolding.

Agriculture: Lightweight yet durable ropes for fencing, irrigation, and crop support.

Adventure and Safety: Ropes designed for climbing, ziplining, and rescue operations.

This wide-ranging utility makes National Ropes a one-stop destination for all rope-related needs.

National Ropes: A Symbol of Trust

In an industry where safety and reliability are paramount, National Ropes has become a trusted name. Their commitment to ISO-certified processes, continuous product innovation, and customer-focused service has earned them a loyal clientele across India and beyond.

Final Thoughts

If you're searching for dependable ropes manufacturers in India, National Ropes deserves to be at the top of your list. With a strong foundation in quality, innovation, and service, National Ropes continues to raise the bar in rope manufacturing. Whether you're a business looking for bulk industrial supplies or a project manager seeking custom solutions, partnering with National Ropes ensures you get ropes that deliver performance, safety, and peace of mind.

0 notes

Text

Synthetic Ropes Market to Soar Owing to Marine Demand

The Global Synthetic Ropes Market is estimated to be valued at US$ 2.12 Bn in 2025 and is expected to exhibit a CAGR of 6.0% over the forecast period 2025 to 2032. Synthetic ropes are engineered from high–strength polymers such as nylon, polyester, and polypropylene, offering superior tensile strength, reduced weight, and excellent resistance to abrasion and chemicals compared with traditional natural fibers. These ropes find widespread applications across marine mooring, offshore drilling, construction lifting, mining haulage, and adventure sports, where safety, durability, and ease of handling drive business growth. The evolving market dynamics reflect increasing emphasis on lightweight solutions in the shipping industry and renewable-energy projects, fueling market growth and shaping industry trends.

Synthetic Ropes Market Insights as advanced manufacturing techniques enable customization of rope diameters, coatings, and load-bearing capacity to meet stringent operational requirements, thereby boosting market demand. As global infrastructure expansion accelerates and offshore wind farms proliferate, synthetic ropes play a critical role in anchoring and cable-laying operations. The versatility of these products not only enlarges the industry size but also opens new market opportunities in emerging economies.

Get more insights on,Synthetic Ropes Market

#Coherent Market Insights#Synthetic Ropes#Synthetic Ropes Market#Synthetic Ropes Market Insights#Polyethylene#Polypropylene

0 notes

Text

Dissolved Air Flotation (DAF) Systems Market Outlook 2025–2031: Global Industry Trends & Forecast

"

The Global Dissolved Air Flotation (DAF) Systems Market report offers detailed insights into the industry, including key facts, figures, and trends. This report explores the entire market structure—from raw material suppliers to manufacturers—while highlighting major market segments. It includes historical data and offers forecasts for the period 2025 to 2031.

Key Highlights:

Recent innovations and scientific research around new Dissolved Air Flotation (DAF) Systems products are examined.

The report also looks at why companies are shifting towards synthetic sourcing methods.

Leading manufacturers and companies in the Dissolved Air Flotation (DAF) Systems industry are analyzed for their strategies, costs, and opportunities for growth.

Major Players in the Dissolved Air Flotation (DAF) Systems Market:

KWI Group

Evoqua Water Technologies

FRC Systems

Benenv

Water Tecnik

Fluence

DAF Corporation

Hyland Equipment Company

WSI International

Toro Equipment

WesTech Engineering

Napier-Reid

MAK Water

VanAire

Kusters Zima

Aries Chemical

Wpl International

Nijhuis Water Technology

Purac

World Water Works

Xylem

This report highlights top companies in the industry and provides an unbiased overview of their latest strategies, product developments, and business plans. It acts as a valuable resource for buyers, investors, and stakeholders planning their next move in the global market.

For more details, visit our full report https://marketsglob.com/report/dissolved-air-flotation-daf-systems-market/640/

Product Types Covered:

Less Than 20 m³/hour

20-50 m³/hour

More Than 50 m³/hour

Applications Covered:

Industrial Application

Municipal Application

Drinking Water Application

Others

Sales Channels Covered:

Direct Channel

Distribution Channel

Regional Insights:

North America (United States, Canada, Mexico)

Europe (Germany, United Kingdom, France, Italy, Russia, Spain, Benelux, Poland, Austria, Portugal, Rest of Europe)

Asia-Pacific (China, Japan, Korea, India, Southeast Asia, Australia, Taiwan, Rest of Asia Pacific)

South America (Brazil, Argentina, Colombia, Chile, Peru, Venezuela, Rest of South America)

Middle East & Africa (UAE, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of Middle East & Africa)

What the Report Offers:

A complete overview of the global Dissolved Air Flotation (DAF) Systems market

Industry trends and forecasts from 2025 to 2031

Analysis of CAGR and market growth potential

New market opportunities and marketing strategies

R&D developments, new product demand, and application trends

Detailed company profiles of key industry players

Insights into product types, cost-effective manufacturing, and competitive analysis

Evaluation of market revenue from both generic and premium product categories

Review of partnerships, licensing, and co-development deals in the industry

The Global Dissolved Air Flotation (DAF) Systems Market report provides deep insights into emerging trends, future growth areas, and investment opportunities. It includes product specifications, production methods, cost structures, and pricing analysis—making it a valuable guide for businesses looking to succeed in this fast-growing market.

" Medicinal Mushroom Extracts Market Polio Vaccine Market Fuel Polishing Carts Market HMPE (High Modulus Polyethylene) Ropes Market Marine Omega-3 Market Titanium Metal (Titanium Alloy) Market Metronidazole Market Digital Printed Wallpaper Market Commercial Kitchen Ventilation Systems Market Plastic Pallet Market Multi-Functional Cooking Food Processors Market Guerbet Alcohols Market Medical Skull CT Market

0 notes

Text

Ropes Market Trends: Rising Demand, Innovations, and Growth Potential in Various Industries

The ropes market has been witnessing steady growth due to increasing demand across multiple industries, including construction, marine, mining, and sports. The rising adoption of advanced materials such as synthetic fibers has revolutionized the industry, enhancing durability, flexibility, and load-bearing capacity. As businesses look for stronger and more sustainable solutions, manufacturers are focusing on technological advancements to meet evolving industry needs. Additionally, the shift toward eco-friendly materials and the development of smart ropes with integrated sensors are gaining traction, signaling a new phase of innovation in the market.

Growing Demand Across Key Industries

Construction and infrastructure development have been significant drivers for the ropes market. With the expansion of urbanization and increasing investments in commercial and residential projects, the demand for high-strength ropes for lifting, rigging, and safety applications has surged. Similarly, the marine and fishing industry continues to rely heavily on durable ropes for mooring, towing, and netting. The mining sector also demands robust ropes capable of handling extreme conditions and heavy loads. Furthermore, the sports and adventure industry has contributed to market growth, particularly with the rising popularity of rock climbing, sailing, and other outdoor activities.

Material Innovations and Technological Advancements

The industry has transitioned from traditional natural fiber ropes to synthetic and hybrid materials, offering superior performance. Materials such as polypropylene, nylon, and high-modulus polyethylene (HMPE) are now widely used due to their lightweight, high strength, and resistance to environmental factors. Innovations in rope manufacturing, such as coated and UV-resistant variants, have further enhanced their lifespan and efficiency. Additionally, the integration of smart technology into ropes, including load monitoring sensors, is providing industries with real-time safety data, improving operational efficiency and reducing accidents.

Sustainability and Environmental Considerations

As sustainability becomes a focal point in manufacturing, the ropes market is shifting towards eco-friendly alternatives. Recyclable and biodegradable ropes are gaining popularity, especially in the marine and agriculture industries, where reducing environmental impact is crucial. Companies are investing in research and development to create ropes that maintain strength and durability while minimizing waste. The use of bio-based polymers and recycled materials is becoming more prevalent, reflecting the industry's commitment to sustainability.

Challenges in the Ropes Market

Despite positive growth trends, the ropes market faces several challenges. Fluctuating raw material prices and supply chain disruptions have impacted production costs and availability. Additionally, competition among manufacturers has intensified, leading to price pressures. The need for continuous product innovation to meet industry-specific demands also presents challenges, as companies must balance cost-effectiveness with performance improvements. Furthermore, counterfeit and low-quality products in the market pose safety risks and affect consumer trust in premium brands.

Regional Market Trends and Growth Opportunities

Asia-Pacific remains a dominant player in the ropes market, driven by rapid industrialization, infrastructure projects, and a strong presence in marine and fishing activities. Countries like China, India, and Japan have witnessed a surge in demand for high-performance ropes in construction and manufacturing sectors. North America and Europe are also significant markets, with increasing investments in advanced rope technology for industrial and recreational applications. The Middle East and Africa are experiencing growth due to expanding oil and gas exploration, where high-strength ropes play a critical role.

Future Outlook and Market Potential

The future of the ropes market looks promising, with increasing demand for lightweight, high-performance, and sustainable rope solutions. Advancements in nanotechnology and material science are expected to further enhance rope properties, making them more efficient for specialized applications. The growing emphasis on workplace safety and stringent regulations will also drive innovation in high-strength and smart ropes. As industries continue to evolve, the market is poised for sustained growth, driven by technological progress, environmental consciousness, and expanding application areas.

0 notes

Text

Offshore Mooring Market

Offshore Mooring Market Size, Share, Trends: Delmar Systems, Inc. Leads

Growing adoption of synthetic mooring systems revolutionizes offshore operations.

Market Overview:

The global Offshore Mooring Market is projected to grow at a CAGR of 3.8% from 2024 to 2031. The market value is expected to increase significantly during this period. The Asia-Pacific region dominates the market, driven by increasing offshore oil and gas exploration activities and growing investments in renewable energy projects. Key metrics include rising deep-water and ultra-deepwater exploration, increasing floating production storage and offloading (FPSO) deployments, and growing focus on offshore wind energy installations.

The offshore mooring sector is rapidly transitioning to the usage of synthetic mooring systems. These systems, made of materials like as polyester and high-modulus polyethylene (HMPE), have various advantages over traditional steel chain and wire rope systems, including reduced weight, increased fatigue resistance, and decreased maintenance requirements. This study is motivated by the need for more efficient and cost-effective mooring methods, especially in deep-water and ultra-deepwater situations. Over the previous three years, the number of new offshore facilities that use synthetic mooring lines has increased by 25 percent. Industry analysts predict that synthetic mooring systems will account for up to 40% of the global offshore mooring market by 2028, indicating a significant shift in the industry.

DOWNLOAD FREE SAMPLE

Market Trends:

The offshore mooring sector is rapidly transitioning to the usage of synthetic mooring systems. These systems, made of materials like as polyester and high-modulus polyethylene (HMPE), have various advantages over traditional steel chain and wire rope systems, including reduced weight, increased fatigue resistance, and decreased maintenance requirements. This study is motivated by the need for more efficient and cost-effective mooring methods, especially in deep-water and ultra-deepwater situations. Over the previous three years, the number of new offshore facilities that use synthetic mooring lines has increased by 25 percent. Industry analysts predict that synthetic mooring systems will account for up to 40% of the global offshore mooring market by 2028, indicating a significant shift in the industry.

Market Segmentation:

FPSOs dominate the offshore mooring industry, accounting for more than YY% of the overall market value. The superiority of FPSOs over fixed platforms stems from their agility, ability to work in remote and deep-water zones, and cost-effectiveness.

The global FPSO market is estimated to reach significant levels by 2031, increasing at a 4.8% CAGR between 2024 and 2031. This growth has a direct impact on the need for offshore mooring systems, as each FPSO requires a robust mooring solution.

Major oil and gas companies are increasing spending for FPSO projects. For example, a major oil company recently announced plans to install five new FPSOs in deep-water sites over the next three years, at a cost of more than USD XX billion. This project alone is expected to generate a demand for around 100 km of mooring lines and related equipment.

The Tension Leg Platform (TLP) market is also growing quickly, particularly in ultra-deepwater applications. TLP use in water depths higher than 1,500 metres increased by 15% year on year in 2023, owing to its ability to provide a consistent platform for drilling and production activities in difficult environments. This trend is expected to continue, with industry analysts projecting a 20% CAGR for TLP mooring systems in ultra-deepwater applications over the next five years.

Market Key Players:

Delmar Systems, Inc.

Mampaey Offshore Industries B.V.

Trelleborg AB

Offspring International Limited

Bluewater Energy Services B.V.

Lamprell Energy Limited

Contact Us:

Name: Hari Krishna

Email us: [email protected]

Website: https://aurorawaveintellects.com/

0 notes

Text

Offshore Mooring Market Emerging Trends Reshaping Marine Anchoring Solutions

The offshore mooring market is witnessing dynamic transformation as technological innovation, environmental imperatives, and expanding offshore projects converge. Mooring systems, which are critical for anchoring floating structures such as oil rigs, FPSOs (Floating Production Storage and Offloading units), and wind turbines, are becoming increasingly sophisticated to meet the growing complexity of marine operations. With energy exploration moving into deeper waters and renewable projects accelerating, the demand for high-performance and reliable mooring systems is expected to grow steadily in the coming years.

Shift Towards Deepwater and Ultra-Deepwater Exploration

One of the primary emerging trends in the offshore mooring market is the rapid shift towards deepwater and ultra-deepwater exploration. As conventional reserves near shore deplete, oil and gas companies are pushing operations into deeper waters, where extreme environmental conditions demand more robust and adaptable mooring systems. These systems must withstand higher pressures, currents, and wave forces, leading to the adoption of advanced materials and engineering designs.

Synthetic ropes and high-tensile mooring lines are gaining traction due to their ability to reduce overall weight while maintaining strength and reliability. Furthermore, vertical load anchors (VLAs) and suction pile anchors are increasingly preferred in deeper environments due to their ease of installation and superior holding capacity.

Expansion of Offshore Renewable Energy Projects

The rise of offshore wind energy is playing a pivotal role in shaping the offshore mooring market. Floating wind turbines, which are ideal for deeper waters where fixed structures are not feasible, require stable and secure mooring systems. This transition is particularly evident in regions such as Europe, North America, and parts of Asia-Pacific, where large-scale investments in floating wind farms are accelerating.

As governments and private investors emphasize low-carbon solutions, the demand for mooring systems that can support floating solar farms and wave energy converters is also increasing. This trend is fostering innovation in mooring configurations, such as catenary and taut-leg systems, to offer better stability with minimal seabed impact.

Digitalization and Remote Monitoring Integration

Another emerging trend is the incorporation of digital technologies for monitoring and maintenance. Advanced sensors, Internet of Things (IoT) devices, and remote monitoring platforms are being deployed on mooring lines and anchors to collect real-time data. This data is used to monitor tension, fatigue, corrosion, and other performance metrics, enabling predictive maintenance and reducing the risk of failures.

Digital twin technology is also being utilized to simulate mooring system performance in various sea states and operational scenarios. By modeling the physical behavior of the mooring systems in a digital environment, companies can enhance design accuracy, reduce downtime, and optimize lifecycle costs.

Sustainability and Environmental Considerations

Environmental sustainability is becoming an integral part of mooring system development. Regulatory bodies are enforcing stricter guidelines regarding seabed disturbance, emissions, and material usage. Consequently, manufacturers and service providers are focusing on eco-friendly designs and recyclable materials.

Biodegradable lubricants, coatings that reduce marine growth, and anchors designed to minimize seabed disruption are becoming standard. Additionally, the use of mooring systems that can be easily removed or repositioned is gaining popularity, particularly in temporary offshore installations and decommissioning projects.

Modular and Hybrid Mooring Solutions

To cater to the varying demands of different offshore installations, there is a growing trend toward modular and hybrid mooring systems. These systems combine elements of different mooring types (such as spread mooring and turret mooring) to deliver optimized performance across a wide range of operational conditions.

Hybrid solutions offer greater flexibility, enabling easy adaptation to changing project requirements or environmental factors. This trend is especially beneficial in emerging offshore oilfields and renewable energy projects where scalability and adaptability are critical.

Regional Developments and Market Expansion

Geographically, Asia-Pacific is emerging as a high-potential region due to expanding offshore energy initiatives, particularly in China, India, Japan, and South Korea. Europe continues to lead in offshore wind energy deployment, while North America is expected to witness strong growth driven by oil & gas exploration and renewable energy mandates.

The Middle East and Africa, with their growing interest in offshore hydrocarbon reserves, are also expected to contribute significantly to the mooring systems demand, especially for floating production and storage units.

Conclusion

The offshore mooring market is undergoing a fundamental shift driven by deeper water projects, the renewable energy boom, and the integration of digital and sustainable technologies. As offshore operations grow more complex and environmentally conscious, mooring systems will need to keep evolving in terms of design, functionality, and performance. Stakeholders who adapt quickly to these emerging trends will be best positioned to thrive in this competitive and rapidly advancing sector.

0 notes

Text

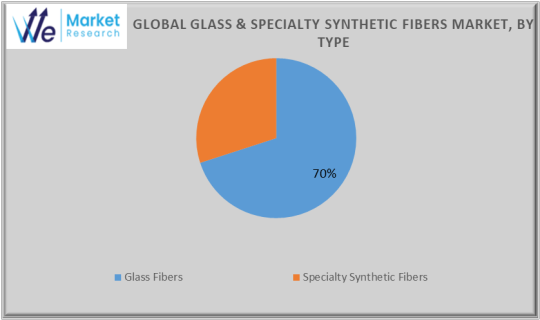

Glass Fibers & Specialty Synthetic Fibers Market Challenges, Analysis and Forecast to 2034

The Glass Fibers & Specialty Synthetic Fibers Market is a dynamic segment within the materials industry, driven by the increasing demand for lightweight, durable, and high-performance materials across various sectors. These fibers are engineered for applications that require superior mechanical properties, thermal stability, and resistance to environmental factors

The market for glass fiber and specialty synthetic fibers is expected to increase at a compound annual growth rate (CAGR) of 6.4% between 2024 and 2034. According to an average growth trend, the market is expected to reach USD 144.58 billion in 2034. The global market for glass fibers and specialty synthetic fibers is expected to generate USD 85.59 billion by 2024.

Get a Sample Copy of Report, Click Here: https://wemarketresearch.com/reports/request-free-sample-pdf/glass-and-specialty-synthetic-fibers-market/1603

Glass Fibers & Specialty Synthetic Fibers Market Growth Drivers

Urbanization and Infrastructure Growth:

Increasing investments in construction and urban development drive demand for glass fibers.

Rising Defense Budgets:

Governments worldwide are increasing investments in protective equipment using synthetic fibers.

Shift Toward Renewable Energy:

Wind energy projects favor glass fibers for turbine blades.

Advancements in Material Engineering:

Innovations are improving the properties and reducing production costs of synthetic fibers.

Specialty Synthetic Fibers: Types

Aramid Fibers:

Examples: Kevlar, Twaron.

High tensile strength and resistance to impact and heat.

Used in bulletproof vests, fire-resistant clothing, and ropes.

Carbon Fibers:

Lightweight and exceptionally strong.

Applications: Aerospace, sports equipment, automotive (luxury cars).

Ultra-High-Molecular-Weight Polyethylene (UHMWPE):

Examples: Dyneema, Spectra.

Extremely lightweight with high impact resistance.

Used in personal armor, fishing lines, and medical implants.

Polybenzimidazole (PBI):

High thermal and chemical stability.

Used in firefighting gear and aerospace insulation.

Polyimide Fibers:

Heat-resistant fibers ideal for use in high-temperature industrial applications.

Glass Fibers & Specialty Synthetic Fibers Market Challenges

High Costs of Specialty Fibers:

The manufacturing process for carbon and aramid fibers is resource-intensive.

Environmental Impact:

Synthetic fibers contribute to pollution if not recycled properly.

Competition from Emerging Materials:

Natural fibers like hemp and bamboo, as well as metal composites, are gaining attention.

Emerging Trends

Integration with Smart Technologies:

Development of fibers with embedded sensors for structural health monitoring.

Circular Economy Initiatives:

Companies are investing in recycling technologies for glass and synthetic fibers.

Hybrid Materials:

Combining glass and synthetic fibers to create composites with enhanced properties.

Glass Fibers & Specialty Synthetic Fibers Market Segmentation,

By Type

Glass Fibers

E-Glass

S-Glass

C-Glass

Others

Specialty Synthetic Fibers

Polyester

Nylon

Aramid

Carbon Fibers

Polypropylene (PP)

Others

By Application

Textile

Construction

Automotive

Aerospace & Defense

Marine

Consumer Goods

Packaging

Wind Energy

Others

Key companies profiled in this research study are,

The Global Glass Fibers & Specialty Synthetic Fibers Market is dominated by a few large companies, such as

Owens Corning

Jushi Group

PPG Industries

Saint-Gobain

China National Glass Industrial Group Corporation (CNG)

Nippon Electric Glass Co., Ltd.

Sika AG

DuPont

Solvay

Teijin Limited

Hyosung Corporation

Toray Industries

DSM (Dutch State Mines)

BASF

Asahi Kasei Corporation

Others

Glass Fibers & Specialty Synthetic Fibers Industry: Regional Analysis

Forecast for the North American market

North America will be a significant player in the glass fiber and specialized synthetic fiber industries, accounting for about 40% of the worldwide market in 2023. Due to its technological dominance and strong industrial base in the automotive, aerospace, and defense sectors, North America has a disproportionate amount. North America, particularly the United States, is a major market for glass fibers and specialty synthetic fibers.

Forecast for the European Market

Europe is an essential market for glass and specialty synthetic fibers due to the prevalence of the automobile and aerospace industries there. Countries like Germany, France, and the UK are investing in lightweight materials for cars and airplanes, which directly increases demand for fibers like glass and carbon fibers. The European Union's focus on sustainability and energy efficiency has led to a greater usage of advanced materials, such as carbon fibers for renewable energy applications like wind turbines and glass fibers for construction. Europe is the hub for research and development, particularly in the areas of lightweight composite materials and high-performance fibers for industrial applications.

Forecasts for the Asia Pacific Market

The growth of the Chinese, Japanese, and Indian industries is primarily responsible for the Asia-Pacific region's sharp increase in demand for glass fibers and specialty synthetic fibers. Particularly in countries like China, India, and Japan, the Asia-Pacific region is fast become increasingly urbanized and industrialized. This is driving the demand for glass fibers in the automotive, infrastructure construction, and building industries. The need for lightweight materials is rising in the Asia-Pacific automotive industry as a result of the rising popularity of electric vehicles (EVs) and fuel-efficient cars in countries like China and Japan. The need for glass and carbon fibers rises as a result.

Conclusion

The Glass Fibers & Specialty Synthetic Fibers Market is poised for robust growth, driven by advancements in material science, the increasing demand for lightweight and high-strength materials, and expanding applications across industries like construction, automotive, aerospace, and renewable energy. While challenges such as high production costs and environmental concerns persist, ongoing innovations in recycling and sustainable fiber production are paving the way for a greener future.

As industries worldwide prioritize efficiency, durability, and sustainability, the market for glass and specialty synthetic fibers is set to play a critical role in shaping the future of materials technology. With strong investments in R&D and the rise of eco-friendly initiatives, this market presents vast opportunities for growth and innovation.

0 notes

Text

Ropes Market Trends Driving Innovations in Materials and Applications Across Multiple Industries Globally

The Ropes Market is witnessing significant transformation, propelled by innovations in material technology and an expanding scope of applications across various industries globally. As industries push for enhanced performance, durability, and safety, the demand for advanced ropes is steadily increasing. This dynamic market landscape offers critical insights into how ropes are evolving beyond their traditional uses to become indispensable in modern industrial and commercial applications.

Innovations in Rope Materials

One of the most influential trends reshaping the ropes market is the development of new and improved materials. Traditional ropes made from natural fibers like cotton, jute, or hemp are gradually being replaced or supplemented by synthetic alternatives and hybrid materials designed to meet rigorous industrial requirements.

High-Performance Synthetic Fibers: Materials such as nylon, polyester, and polypropylene offer superior tensile strength, abrasion resistance, and environmental durability. These synthetics are lightweight yet strong, making them ideal for demanding applications such as marine operations and heavy construction.

Advanced Specialty Fibers: Aramid fibers (e.g., Kevlar) and Ultra-High Molecular Weight Polyethylene (UHMWPE) fibers bring extreme strength-to-weight ratios and resistance to heat and chemicals. These are crucial in aerospace, military, and safety gear manufacturing.

Hybrid and Composite Ropes: Combining natural and synthetic fibers optimizes cost and performance. These ropes deliver balanced flexibility and strength, suited for agricultural, recreational, and general industrial use.

The adoption of these materials enables manufacturers to tailor rope products to specific industry needs, enhancing functionality and lifespan.

Expanding Applications Across Industries

The versatility of ropes today extends well beyond basic binding and lifting. Their applications have expanded widely, driving demand in several key sectors:

Maritime and Shipping: Ropes are essential for mooring, towing, and lifting. The harsh marine environment requires ropes with excellent resistance to saltwater corrosion, UV radiation, and mechanical wear.

Construction and Infrastructure: Ropes used in lifting, rigging, and scaffolding demand high strength and durability. Innovations allow safer handling of heavy materials and machinery.

Agriculture: Durable ropes assist in baling, tethering, and securing loads, often exposed to extreme weather conditions. Biodegradable rope options are gaining traction for eco-conscious farmers.

Sports and Recreation: Climbing ropes, safety harnesses, and sailing ropes benefit from lightweight, strong, and flexible materials, enhancing safety and performance.

Industrial Manufacturing: Specialized ropes are incorporated into conveyor systems, lifting equipment, and safety harnesses, where reliability and compliance with standards are paramount.

Key Market Drivers

The growth trajectory of the ropes market is supported by several important drivers:

Urbanization and Infrastructure Growth: Expanding urban development fuels demand for durable construction materials, including high-quality ropes.

Rising Safety and Compliance Standards: Regulatory pressures compel industries to adopt ropes that meet stringent safety criteria, boosting demand for advanced materials.

Technological Advancements: Incorporation of coatings and smart fibers improves resistance to wear and tear and enables monitoring of rope integrity in critical applications.

Sustainability Initiatives: Increasing awareness about environmental impact leads to the development of biodegradable and recyclable rope options, aligning with global eco-friendly trends.

Challenges and Market Outlook

Despite promising growth, the ropes market faces certain challenges:

Raw Material Price Volatility: Fluctuations in synthetic fiber costs can affect manufacturing expenses and pricing strategies.

Intense Competition: The market includes numerous players offering a wide range of products, leading to pricing pressure and the need for continuous innovation.

Technological Integration: Developing smart ropes with embedded sensors requires significant investment and expertise, which may limit adoption in some regions initially.

Nonetheless, the future outlook is positive. The market is expected to witness sustained growth with innovations focusing on smart ropes integrated with IoT technology for real-time condition monitoring, enhanced durability, and safety features.

Summary of Key Points:

Innovative materials such as synthetic fibers, aramid, and UHMWPE are transforming rope performance.

Applications span maritime, construction, agriculture, sports, and manufacturing sectors.

Market growth driven by urbanization, safety standards, technological advances, and sustainability trends.

Challenges include raw material costs and competitive pressures.

Emerging trends include smart ropes with real-time monitoring and eco-friendly materials.

The Ropes Market is positioned to redefine traditional applications with material innovation and technology, delivering solutions that cater to evolving industry needs across the globe.

#RopesMarket#MaterialInnovation#IndustrialApplications#SustainableMaterials#SmartRopes#GlobalIndustryGrowth

0 notes

Text

Baling Twines Market: Comprehensive Insights and Growth Outlook

The global Baling Twines Market play a vital role in agriculture and industrial packaging, offering a reliable and efficient solution for bundling hay, straw, crops, and grasses. Their strength, durability, and ease of use make them an indispensable tool for farmers and logistics providers alike. As agricultural practices become increasingly mechanized and sustainable practices gain momentum, the baling twines market is positioned for significant growth.

In 2023, the global baling twines market was valued at $430 billion. With a compound annual growth rate (CAGR) of 6.00%, it is projected to reach $750 billion by 2030. This blog dives into the market’s current landscape, future prospects, key drivers, challenges, and trends that define its trajectory.

Market Overview

Key Metrics

Base Year: 2023

Market Size in 2023: $430 billion

Projected Size in 2024: $510 billion

Projected Size in 2030: $750 billion

CAGR (2024–2030): 6.00%

The market’s growth is fueled by rising global food demand, advancements in farming technology, and increasing adoption of sustainable materials.

Segmentation Analysis

1. By Type

Baling twines are categorized into two primary types, each tailored to specific requirements:

PP (Polypropylene):

Polypropylene twines dominate the market due to their superior strength, resistance to UV rays, and durability.

They are widely used in large-scale farming and industrial applications where reliability is critical.

Natural Fibers:

As environmental concerns rise, the demand for biodegradable twines made from natural fibers such as sisal and jute is increasing.

These twines are ideal for eco-conscious operations and applications that prioritize sustainability.

2. By Application

The applications of baling twines span various sectors, with agriculture being the largest:

Crops: The most significant application, crops require baling twines for securely bundling hay, straw, and other materials. Farmers rely on high-tensile twines to ensure transport and storage safety.

Grasses: Used in bundling grasses for livestock feed, turf production, and landscaping, this segment also contributes significantly to the overall demand for baling twines.

Key Market Players

The baling twines market is competitive, with manufacturers striving to meet diverse industry demands while addressing environmental concerns. Key players include:

Cotesi: A global leader offering high-quality synthetic baling twines.

Tama: Known for its innovative agricultural packaging solutions.

Filpa and Exporplas: Experts in durable polypropylene twines.

PIIPPO and Asia Dragon Cord & Twine: Producers of eco-friendly natural fiber twines.

Karatzis and Sicor: Focused on advanced materials and versatile products.

Quanxiang and Xingtai Jiuxin: Dominant players in the Asia Pacific market.

UPU Industries Ltd and T&H Packaging: European leaders delivering cutting-edge twine solutions.

Azuka Ropes & Twines and Cordexagri: Renowned for their innovation and regional reach.

These companies are investing in research and development to create durable, cost-effective, and environmentally sustainable solutions.

Regional Insights

1. North America

Dynamics: High levels of agricultural mechanization and the adoption of advanced farming practices make North America a significant market.

Trends: Demand for UV-resistant polypropylene twines is growing due to variable weather conditions across the region.

2. Europe

Dynamics: Europe’s mature market is driven by strict environmental regulations encouraging the use of biodegradable baling twines.

Focus: Leading manufacturers are innovating to produce eco-friendly products that comply with these regulations.

3. Asia Pacific

Dynamics: Rapid growth in the agriculture sector, particularly in China and India, is driving demand for baling twines.

Challenges: The price-sensitive nature of the region’s markets requires manufacturers to balance cost and quality.

4. Latin America

Dynamics: With an emphasis on sugarcane and hay farming, Latin America offers a growing market for baling twines.

Opportunities: Export-oriented agricultural practices open doors for regional manufacturers to expand their reach.

5. Middle East & Africa

Dynamics: Emerging economies in this region are adopting modern agricultural techniques, boosting demand for baling twines.

Challenges: Limited infrastructure and high import costs could hinder market growth in certain areas.

Market Drivers

1. Rising Global Food Demand

The growing global population requires increased agricultural output, driving demand for efficient baling solutions for crops and grasses.

2. Advancements in Farming Practices

The adoption of mechanized farming equipment, such as balers, has created a need for strong and reliable baling twines.

3. Sustainability Initiatives

The push towards environmentally friendly practices has led to the development of biodegradable and recyclable twines, boosting market growth.

4. Versatility Across Industries

While agriculture is the primary driver, industrial sectors such as logistics, horticulture, and landscaping also contribute to the demand for baling twines.

5. Regional Growth Opportunities

Emerging markets in Asia Pacific, Latin America, and Africa present untapped potential for manufacturers looking to expand their reach.

Challenges

1. Environmental Concerns

The environmental impact of synthetic materials like polypropylene has led to stricter regulations, increasing production costs.

2. Fluctuating Raw Material Costs

Variability in the cost of raw materials can affect pricing strategies and profit margins for manufacturers.

3. Regional Disparities

While developed regions have embraced advanced baling solutions, emerging markets face challenges such as limited access to modern farming equipment.

4. Competition from Alternative Solutions

Innovations in packaging and bundling materials pose a threat to traditional baling twines.

5. Supply Chain Issues

Disruptions caused by geopolitical tensions and global pandemics can impact the availability of raw materials and final products.

Emerging Trends and Opportunities

1. Eco-Friendly Innovations

The focus on sustainable agriculture has encouraged manufacturers to develop biodegradable twines, aligning with environmental regulations and consumer preferences.

2. Product Customization

Tailored solutions, such as color-coded twines for different crops, are gaining popularity among end-users.

3. Integration with Smart Farming

The integration of baling twines with IoT-enabled smart farming solutions can improve efficiency and reduce waste.

4. Expansion into Emerging Markets

Untapped regions in Africa, Southeast Asia, and Latin America offer immense growth potential, especially for natural fiber twines.

5. Partnerships and Collaborations

Collaborating with equipment manufacturers and agricultural organizations can help manufacturers enhance product visibility and adoption.

Future Outlook

The baling twines market is set to experience sustained growth as global agriculture continues to evolve. Technological advancements, sustainability trends, and the expanding applications of baling twines across industries will drive demand. The market’s robust CAGR of 6.00% reflects its adaptability to changing market dynamics and consumer needs.

Conclusion

The baling twines market is an integral part of modern agriculture and industrial operations. Its ability to adapt to sustainability challenges, coupled with advancements in material science and technology, positions it for a bright future. With a projected market size of $750 billion by 2030, the industry is well-equipped to meet the demands of a growing global population and an evolving agricultural landscape.

Browse More:

Best Cast Iron Dosa Tawa

0 notes

Text

Key Drivers Fueling Growth in the Aramid Fiber Market

The global aramid fiber market was estimated at USD 4.09 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 8.1% from 2024 to 2030. This growth is largely attributed to rising demand from various industries, including oil and gas, healthcare, and manufacturing. The increasing focus on workplace safety, driven by stringent government regulations, is anticipated to further fuel market expansion throughout the forecast period.

However, the market experienced sluggish growth during the COVID-19 pandemic, primarily due to a decline in demand from the industrial sector. Government-imposed restrictions led to temporary shutdowns across a wide range of industries, significantly limiting market activity during that period.

Gather more insights about the market drivers, restrains and growth of the Aramid Fiber Market

Market Dynamics

Aramid fibers are renowned for their strength, synthetic nature, and heat resistance. These advantageous properties make them highly desirable in military and aerospace applications, particularly for ballistic-grade body armor fabric. One of the key features of aramid fibers is that they neither ignite nor melt under typical levels of oxygen, which provides excellent flame and heat resistance. Additionally, aramid fibers serve as substitutes for metal wires and organic fibers in structural composite applications, particularly in ropes used on oil rigs, marine and aerospace industries, automobiles, and bulletproof vests. Their superior mechanical properties—5% to 10% higher than those of other synthetic fibers—enhance their applicability in these demanding environments.

The aramid fiber industry is continuously evolving, with ongoing efforts to develop and manufacture synthetic fibers that meet the demands of new technologies. This includes replacing asbestos, which is known to be carcinogenic and toxic. Aramid fibers contribute strength and wear resistance to friction materials that do not contain asbestos. They allow for the selection of inert fillers based on thermal and wear characteristics, minimizing concerns related to the physical properties of those fillers. While asbestos is strong and can withstand chemical and high-temperature exposure, making it relatively inexpensive compared to other materials, its hazardous nature makes it a less desirable option in many applications.

Aramid fibers are used in two main types of applications: reinforcement in composites and fabrics in clothing. In the composite sector, they are utilized in military vehicles, sports goods, and aircraft. In the fabric sector, aramid fibers are crucial in creating protective clothing, such as bulletproof vests and fire-resistant garments. They are extensively employed across various applications, including protective gloves, sailcloth, flame- and cut-resistant clothing, snowboards, helmets, filament-wound pressure vessels, body armor, optical fiber cable systems, ropes and cables, tire reinforcement, rubber goods, tennis strings, hockey sticks, jet engine enclosures, asbestos replacement, and circuit board reinforcement.

In the U.S. market, growth is expected to be driven by the increased adoption of advanced material handling equipment, such as wagon tipplers, belt conveyor systems, and bucket elevators. These innovations facilitate the efficient movement and handling of materials, particularly within the cement industry. Additionally, the trend towards zero-labor warehousing has led to the adoption of advanced robotic systems, which is expected to further benefit market growth. Protective gear designed to safeguard workers from risks associated with hazardous jobs and challenging environmental conditions is another critical aspect of the aramid fiber market.

A significant portion of this protective gear is specifically engineered to shield employees from infections and pollution. Various end-use industries, including manufacturing, oil and gas, mining, healthcare, construction, and military, extensively utilize protective apparel. The ongoing increase in both onshore and offshore drilling activities, along with the expansion of the shale oil and gas industry, is expected to drive demand for aramid fibers in the U.S. market.

Among the different types of aramid fibers, the para-aramid fiber segment is projected to witness significant growth. This increase is attributed to the rising demand for para-aramid fibers across various applications, driven by their rigid molecular structure, which enhances their performance in demanding environments. As industries continue to recognize the value of aramid fibers in enhancing safety and performance, the market is well-positioned for robust growth in the coming years.

Order a free sample PDF of the Aramid Fiber Market Intelligence Study, published by Grand View Research.

#Aramid Fiber Market#Aramid Fiber Market Analysis#Aramid Fiber Market Report#Aramid Fiber Industry#Aramid Fiber Market Dynamics

0 notes

Text

The Ultra High Molecular Weight Polyethylene (UHMWPE) Rope Market is projected to grow from USD 235.7 million in 2023 to an estimated USD 455.7 million by 2032, registering a compound annual growth rate (CAGR) of 8.59% from 2024 to 2032. Ultra High Molecular Weight Polyethylene (UHMWPE) ropes have been gaining significant attention across various industries due to their high-performance attributes. Known for their remarkable strength, durability, and lightweight characteristics, UHMWPE ropes are designed to outperform traditional materials like steel and other synthetic fibers. The market for UHMWPE ropes has been on a steady rise in recent years, driven by growing demand from marine, defense, aerospace, oil & gas, and sports industries. This article explores the key drivers, trends, and future opportunities in the UHMWPE rope market.

Browse the full report at https://www.credenceresearch.com/report/ultra-high-molecular-weight-polyethylene-rope-market

Market Drivers

1. Rising Demand from the Marine Industry: The marine sector has been one of the largest consumers of UHMWPE ropes due to their lightweight and high-strength properties. Applications such as mooring lines, towing ropes, and winches rely heavily on the performance characteristics of these ropes. Additionally, UHMWPE ropes are highly resistant to UV radiation and saltwater, making them a suitable choice for long-term use in maritime environments. As global trade and shipping activities increase, the demand for reliable, durable marine ropes is expected to grow, pushing the UHMWPE rope market upward.

2. Growth in Offshore Oil & Gas Exploration: The offshore oil and gas industry is another significant driver of the UHMWPE rope market. Exploration and drilling activities require equipment that can perform reliably in harsh, remote environments. UHMWPE ropes are used in various offshore applications, such as anchor handling, platform positioning, and rigging operations. Their ability to withstand extreme loads and harsh environmental conditions makes them an ideal choice for these industries. The expansion of offshore oil drilling projects, particularly in regions like the Gulf of Mexico, the North Sea, and offshore Brazil, is expected to drive the demand for UHMWPE ropes further.

3. Defense and Aerospace Applications: In the defense and aerospace sectors, UHMWPE ropes are used for critical applications, including parachute lines, helicopter slings, and high-strength tethering systems. These industries require materials that offer high performance with minimal weight, which makes UHMWPE ropes a preferred option. As defense budgets increase worldwide and demand for advanced aerospace technologies rises, the UHMWPE rope market is expected to see continued growth.

4. Sports and Recreational Use: UHMWPE ropes are also gaining traction in sports and recreational activities, particularly in sailing, rock climbing, and paragliding. The ropes' strength-to-weight ratio, low water absorption, and ease of handling make them ideal for outdoor sports enthusiasts. As these activities become more popular globally, demand for UHMWPE ropes is likely to increase.

Market Trends and Innovations

The UHMWPE rope market is witnessing several emerging trends that are likely to shape its future growth trajectory. These include:

- Sustainability and recycling initiatives: As industries focus more on sustainability, the production of UHMWPE ropes with environmentally friendly practices is becoming more important. Manufacturers are increasingly looking for ways to reduce the carbon footprint of their products and promote recycling initiatives. - Technological advancements: Innovations in manufacturing processes are leading to the development of even stronger and more durable UHMWPE ropes. This includes the use of new coatings and treatments that improve resistance to wear, heat, and UV degradation, further extending the ropes’ lifespan.

- Customization and specialized products: With growing demand from diverse industries, there is an increasing focus on developing customized UHMWPE rope solutions tailored to specific requirements. For example, specialized ropes for extreme environments like deep-sea exploration or high-altitude aerospace applications are seeing growing interest.

Challenges

Despite its numerous advantages, the UHMWPE rope market faces some challenges, including high initial costs compared to traditional materials like steel or polyester ropes. Additionally, although UHMWPE ropes are highly durable, they are sensitive to high temperatures, which can limit their use in certain industrial applications.

Future Outlook

The future of the UHMWPE rope market looks promising, with steady growth anticipated in the coming years. According to market analysts, the global UHMWPE rope market is expected to witness a compound annual growth rate (CAGR) of 7% to 9% over the next decade. This growth will be driven by increasing demand from key industries such as marine, oil & gas, defense, and aerospace, along with innovations in product development.

Key players

Marlow Ropes Ltd.

Yangzhou Hyropes Co., Ltd.

Taizhou Hongda Rope & Net Co., Ltd.

Katradis Marine Ropes Ind. S.A.

Samson Rope Technologies, Inc.

Southern Ropes

Dynamica Ropes ApS

Cortland Limited

Teufelberger Holding AG

Yale Cordage Inc

Segments

Based on Product Type

3 Strands

8 Strands

12 Strands

Based on Application

Oil & Gas

Construction

Marine

Military & Aviation

Mining

Others

Based on Region

North America

U.S.

Canada

Mexico

Europe

Germany

France

U.K.

Italy

Spain

Rest of Europe

Asia Pacific

China

Japan

India

South Korea

South-east Asia

Rest of Asia Pacific

Latin America

Brazil

Argentina

Rest of Latin America

Middle East & Africa

GCC Countries

South Africa

Rest of the Middle East and Africa

Browse the full report at https://www.credenceresearch.com/report/ultra-high-molecular-weight-polyethylene-rope-market